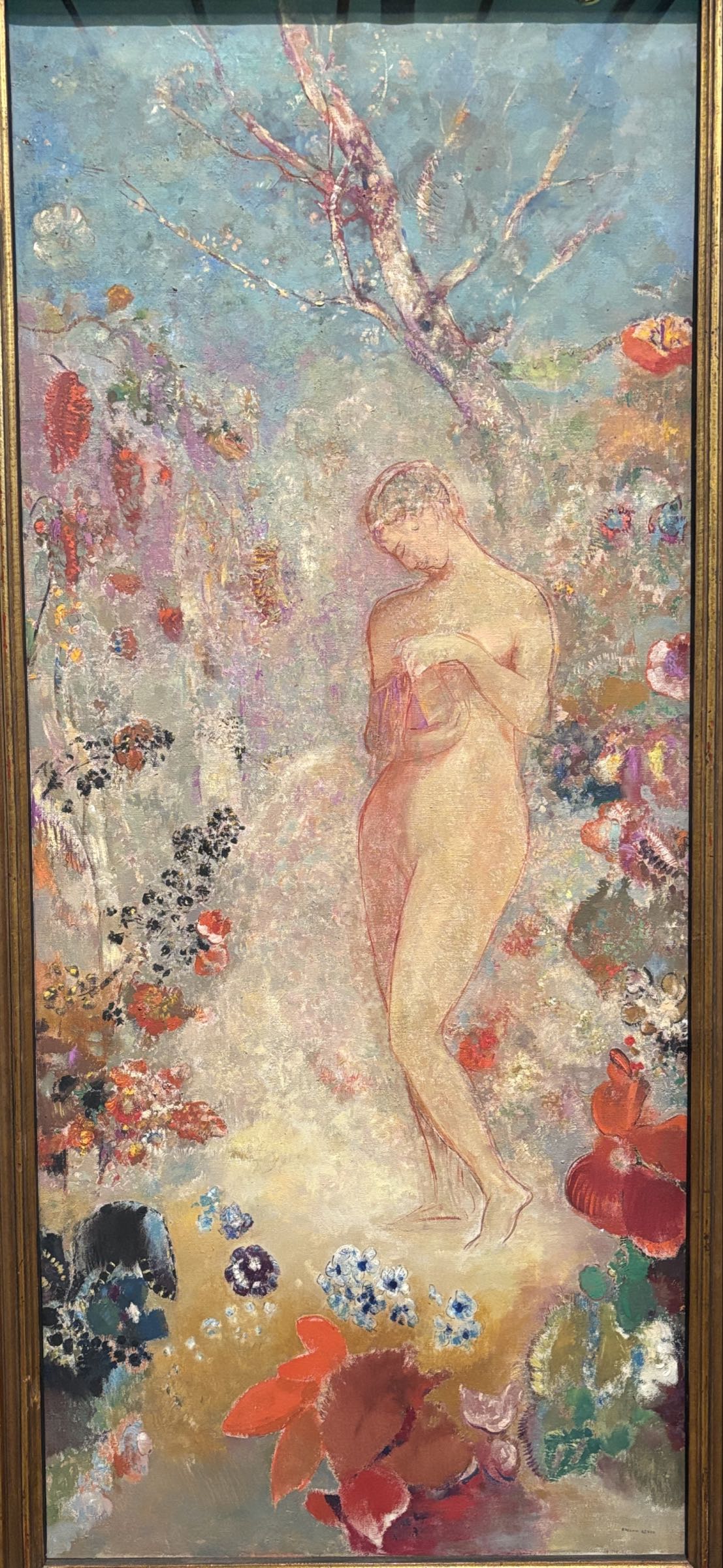

Blue Chip

Jeff Koons

Balloon Dog (Blue), 2021

Blue Chip Will Always Find a Way

In November 2023, a Basquiat sold at Christie's for just over 67 million dollars, a number that would have seemed extraordinary even a decade ago but now reads almost as confirmation rather than surprise. The market for blue chip art has developed a particular grammar of its own: it speaks in nine figures for the very top tier, it speaks in waiting lists and provenance trails and institutional loans, and it speaks in the quiet confidence of collectors who know that certain names have moved beyond fashion into something closer to permanence. What makes that Basquiat result interesting is not the number itself but what surrounded it. The room was attentive in a way that felt different from the speculative fever of 2021.

This was conviction buying, not momentum chasing. The term blue chip borrows from finance, and the borrowing is apt in ways that go beyond the obvious. In equities, blue chip status describes companies with long records of stability, recognizable names, and the kind of liquidity that allows you to move in and out without catastrophic loss. In art, the parallel holds surprisingly well.

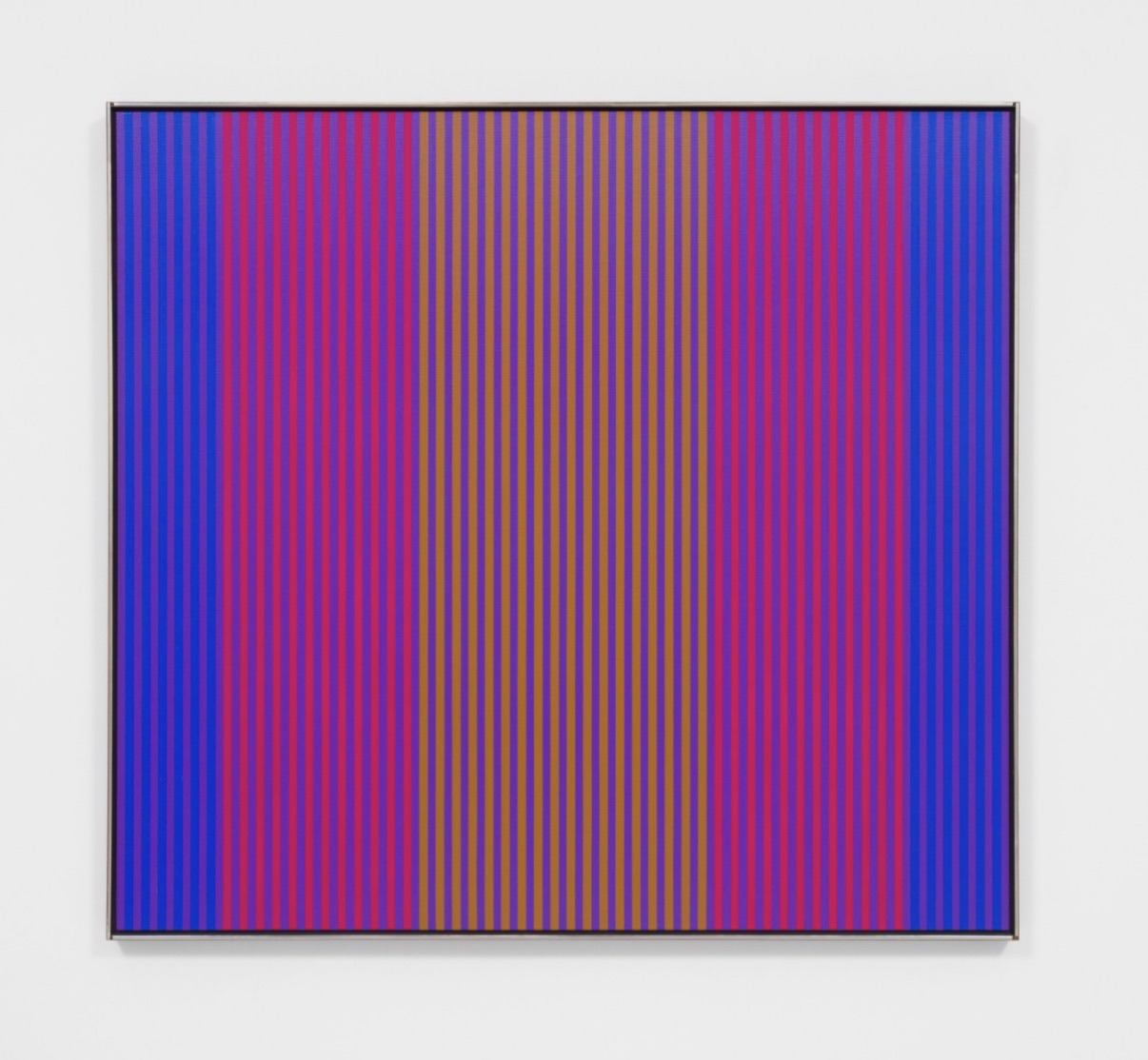

David Hockney

Yosemite I, October 16th 2011, 2011

David Hockney, whose market has shown almost no meaningful weakness across six decades of career, exemplifies the category in its purest form. His retrospective at Tate Britain in 2017 drew some of the largest attendance figures the institution had recorded in years, and the critical conversation around that show did something interesting: it reframed Hockney not as a beloved populist but as a genuinely rigorous formal thinker whose engagement with perspective, light, and photographic seeing deserved serious theoretical attention. The market had always known this. The critical establishment took a little longer to catch up.

Andy Warhol remains the axis around which so much blue chip market logic turns. The Andy Warhol Foundation continues to shape supply in ways that matter enormously to collectors, and Warhol's prices at auction have shown a consistent ability to reset upward whenever a truly fresh example reaches the market. The Tate Modern retrospective of 2020, though complicated by pandemic closures, still generated significant critical writing and renewed museum acquisition interest. What Warhol represents in the blue chip conversation is the idea of an artist whose work operates simultaneously as cultural artifact, philosophical proposition, and liquid asset.

Andy Warhol

Self-Portrait

Very few artists achieve all three simultaneously. Warhol did it so completely that the question of which function matters most has become genuinely interesting to argue about. The institutional collecting picture tells you a great deal about where confidence lives. The Museum of Modern Art has deepened its holdings of Jasper Johns over the past decade, partly in recognition of the fact that his work continues to generate new scholarship rather than simply recirculating old arguments.

The Guggenheim Bilbao mounted a significant Richard Serra installation survey that reminded a younger generation of collectors what scale and material intelligence can accomplish. Ellsworth Kelly's late shaped canvas work, which seemed almost too quiet for a moment dominated by maximalism, has found renewed institutional appetite, with the Glenstone Museum in Maryland treating his legacy with the kind of long form curatorial attention that shifts perception gradually but durably. These institutional moves are not decorative. They are signals, and experienced collectors read them as such.

Roy Lichtenstein

untitled

The critical conversation around blue chip art has become more interesting precisely because it has become more contested. For a period in the early 2010s, there was a tendency to treat canonical status as self evident and the market as a simple validator of existing hierarchies. Writers like Peter Schjeldahl brought genuine skepticism to that assumption, and his long run at The New Yorker consistently asked whether received greatness was actually experienced greatness in the encounter with specific works. Frieze and Artforum have both published sharp revisionary pieces about figures like Francis Bacon and Roy Lichtenstein, not to diminish them but to ask more precise questions about what exactly makes them indispensable.

Bacon's prices remain extraordinary, with works regularly exceeding 50 million dollars at auction, but the most interesting recent scholarship focuses less on his biographical drama and more on his relationship to photographic sources and to continental philosophy. Raoul Dufy occupies an unusual position in this landscape and is worth pausing on. His market is substantial and his museum presence consistent, but critical opinion has been genuinely divided about where he belongs in the modernist canon. The Musée d'Art Moderne de Paris has treated him as a serious figure rather than a decorative one, and there is a growing sense among certain curators that his handling of color and light anticipates later developments that we tend to attribute to other lineages.

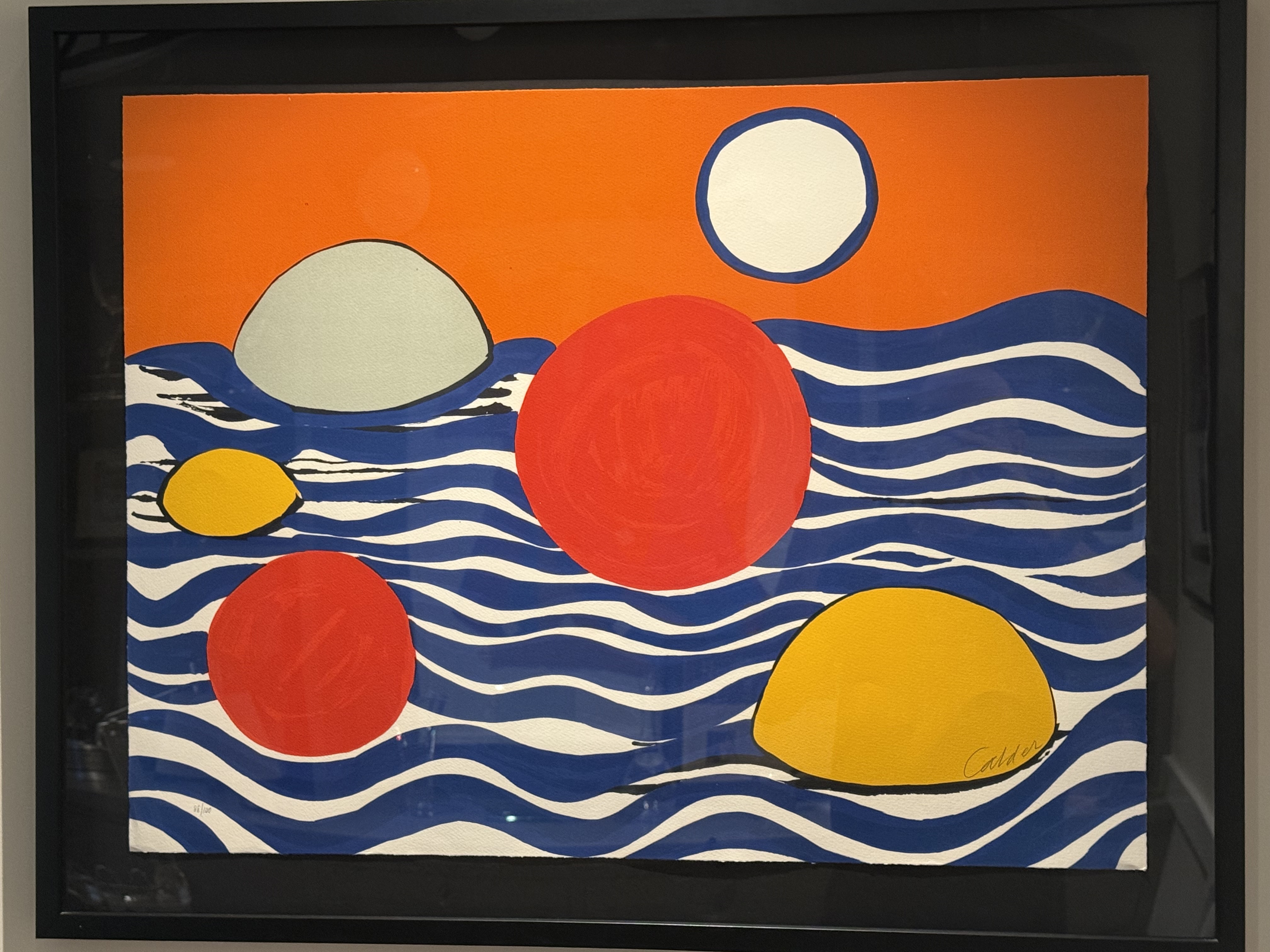

Alexander Calder

Waves and Circles, 1975

Alexander Calder, whose market has strengthened considerably as sculpture has found renewed collector enthusiasm, represents a different version of blue chip permanence: deeply beloved, institutionally secure, and capable of producing auction surprises when a particularly strong mobile or stabile comes to market. Yayoi Kusama's trajectory is perhaps the most instructive recent story in the blue chip category because it illustrates how institutional embrace and popular enthusiasm can reinforce each other without either diminishing the work. Her retrospective organized by the Centre Pompidou and traveling through Europe and North America between 2011 and 2012 positioned her not as a spectacle but as a rigorous conceptualist with a fifty year commitment to ideas about repetition, infinity, and selfhood. The market responded accordingly.

Works that seemed generously priced in 2010 look entirely logical now, and the collector base for Kusama has broadened in ways that tend to create durable demand rather than speculative spikes. Where does the energy move from here. The honest answer is that the blue chip category has become interesting again precisely because it is not monolithic. Wolfgang Tillmans bringing photography fully into the room at these price levels, Gerhard Richter commanding results that rival painting's most celebrated names, Peter Alexander gaining serious institutional recognition on the West Coast: these are not afterthoughts to the category but active arguments about what the category means and where its edges are.

The works on The Collection reflect this breadth deliberately. Blue chip is not a fixed list. It is a conversation about which artists will still matter when fashion has moved on, and that conversation, properly conducted, is one of the most rewarding things serious collecting can offer.